Federal judge throws out Coinbase customer's legal challenge against IRS data request

A federal district court has thrown out a legal challenge from a Coinbase customer seeking to prevent the IRS from accessing his financial data, citing his failure to properly serve notice to all necessary federal officials.

On Wednesday, a federal court in California threw out a legal petition from a Coinbase customer who sought to prevent the IRS from obtaining his financial information, marking at least the second instance within the last twelve months where such a challenge has been dismissed before reaching trial proceedings.

In May 2025, Roger Metz submitted a legal petition to the Northern District of California seeking to invalidate an IRS summons that demanded Coinbase provide his financial documentation related to the examination of his federal tax filing for the year 2022.

Legal counsel representing Metz maintained that the summons infringed upon his constitutional privacy protections, exceeded reasonable scope, and did not satisfy fundamental administrative standards.

Attorneys for Metz further argued that when the IRS delivered the summons in 2024, Metz had already discovered the mistake on his own initiative, submitted a corrected tax return, and remitted the outstanding tax amount.

On Wednesday, US District Judge Araceli Martínez-Olguín issued a ruling against Metz, determining that he had not properly served notice to all mandatory government officials of his petition within the required 90-day timeframe, and threw out the case based on procedural deficiencies.

According to the Federal Rules of Civil Procedure, parties named as defendants must receive formal service of legal actions to guarantee they are informed and given the chance to provide a response. When bringing suit against the federal government in this instance, three separate parties needed to be notified within a 90-day period following the filing: the regional US Attorney serving the relevant district, the US Attorney General headquartered in Washington, D.C., and the particular government agency facing the legal challenge.

Petition thrown out due to "insufficient service of process"

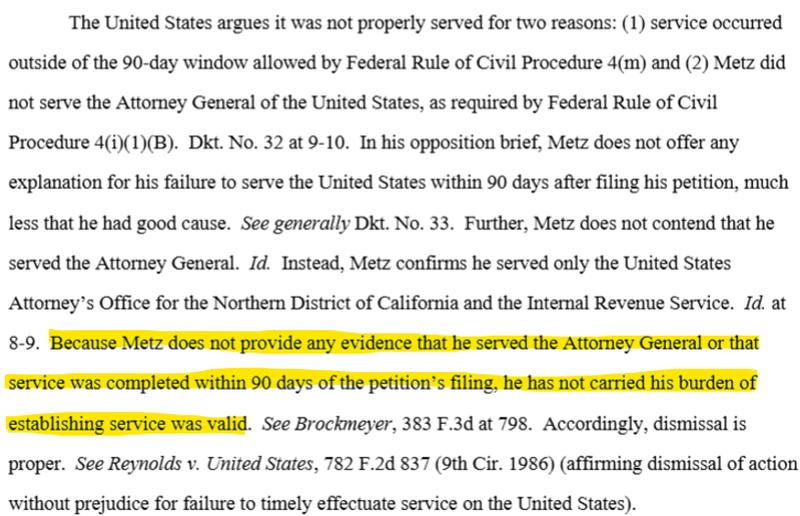

According to court documentation, Metz confirmed he had served both the US Attorney's Office for the Northern District of California and the IRS, but conceded that he had not provided notification to the US Attorney General in Washington within the mandated 90-day timeframe. Federal government attorneys contended this constituted adequate justification for dismissal.

In his opposition brief, Metz does not offer any explanation for his failure to serve the United States within 90 days after filing his petition, much less that he had good cause.

Judge Araceli Martínez-Olguín

Dismissal of a case is proper when there is insufficient service of process.

The petition was dismissed without prejudice, which means Metz retains the option to submit an identical petition in the future.

Cryptocurrency platforms must provide customer information to taxation authorities

Leading cryptocurrency exchanges face legal obligations to gather customer data and disclose taxable earnings to the IRS, as explained by Miles Brooks, who serves as the director of tax strategy at CoinLedger, a tax software company.

The federal tax agency also has the authority to issue "John Doe Summons," which serve to identify broad categories of unnamed taxpayers by legally requiring cryptocurrency exchanges to provide customer records matching certain criteria, such as individuals who executed transactions totaling $20,000 or greater during the period spanning 2016 through 2020.

In a similar legal matter from last year, James Harper claimed the IRS had violated his Fourth Amendment constitutional protections after the tax agency utilized a John Doe Summons to obtain his information from a cryptocurrency exchange. The Supreme Court refused to review his case.