Former OECD Expert: DeFi's Tax Exemption in Europe is Temporary

While DAC8 and CARF currently exclude DeFi from reporting requirements, emerging AML enforcement patterns indicate this exemption may be short-lived, explains Taxbit's Colby Mangels.

The cryptocurrency tax reporting infrastructure recently implemented by the European Union focuses on mechanisms that can be enforced right away, which means decentralized finance (DeFi) remains beyond its current reach.

An ex-official from the Organization for Economic Co-operation and Development (OECD) who contributed to developing the Crypto Asset Reporting Framework (CARF) explained that this exclusion represents a strategic prioritization rather than an oversight.

"It doesn't make sense to go to your grandma and ask her to give you all the tax reporting on crypto just because you happened to work with her over a certain period," Colby Mangels, Taxbit's global head of government solutions and a former OECD adviser, told Cointelegraph. "You really have to go to the intermediaries that are doing this as a business."

Enacted within the EU through the eighth revision of the Directive on Administrative Cooperation (DAC8), these regulations mandate that cryptocurrency exchanges and custodial services start gathering user transaction data beginning in 2026. As centralized exchanges gear up for these new compliance requirements, DeFi platforms remain mostly exempt, resulting in a disparate regulatory environment across the cryptocurrency sector.

How global crypto tax reporting is being rebuilt

Regulations governing cryptocurrency tax reporting are often referenced using various interconnected abbreviations, though these terms should not be treated as synonymous.

The Common Reporting Standard (CRS) represents the OECD's mechanism for automated information sharing among tax authorities, brought into EU law via DAC2. The CRS excludes the majority of cryptocurrency transactions, creating a void now addressed by the CARF.

The CARF represents the OECD's standardized approach to crypto tax reporting. It defines which entities must report, what data must be gathered and the methods for exchanging this information among tax authorities. Nations committed to these data exchanges have begun implementing domestic regulations like the EU's DAC8.

DAC8 marks the EU's initial unified tax transparency system that expands cross-border reporting requirements to cryptocurrency service providers. Built upon the CARF foundation, EU member states faced a Dec. 31 deadline for incorporating this directive into their domestic legislation. DAC8 effectively harmonizes EU nations with the CARF, though individual members may adopt varying implementation schedules at the OECD level.

The EU's implementation corresponds with worldwide adoption of the CARF, as numerous countries prepare to establish tax information sharing systems. Mangels remembered a significantly different landscape approximately 30 years ago. If someone wished to establish a bank account in a foreign jurisdiction, they needed to physically transport cash, travel internationally and meet with banking representatives in person.

"That's a lot of steps to take; so, only people who were really motivated or had the resources would actually do that. That's what we saw in traditional tax evasion cases," Mangels said.

With cryptocurrency technology, traders can hypothetically remain at home, connect to an exchange platform located anywhere globally and begin conducting transactions.

"If I never tell my tax authority where I'm situated — for example, in France — and I never tell them about the money I made trading crypto on an exchange in Singapore, they won't know. They'll have no idea," Mangels added.

Through DAC8 provisions, cryptocurrency trading platforms and custodial service providers must gather standardized client information linked to tax residency status and submit consolidated transaction records to their respective national tax agencies. This data subsequently gets shared internationally.

DeFi is out of scope, but AML trends could change that

DAC8 alongside CARF function as tax disclosure frameworks, yet they overlap with Anti-Money Laundering (AML) issues stemming from insufficient international oversight in cryptocurrency markets.

The OECD creates international benchmarks for taxation and fiscal policy, whereas the Financial Action Task Force (FATF) operates as an independent organization establishing guidelines for AML and combating terrorism financing, both now applicable to crypto markets. Tax collection agencies regularly reference AML structures when establishing definitions that shape reporting regime architecture.

"An interesting fact to know is that the FATF sits in the same offices as the OECD, so you can literally go down the hall or have a coffee with folks there," said Mangels, highlighting the close working relationship between the two bodies.

This collaborative relationship clarifies why DeFi currently falls outside tax reporting mandates. Presently, reporting duties are allocated to recognizable intermediaries conducting transactions as commercial operations. Within most DeFi ecosystems, no centralized operator exists and no custodial arrangement is present.

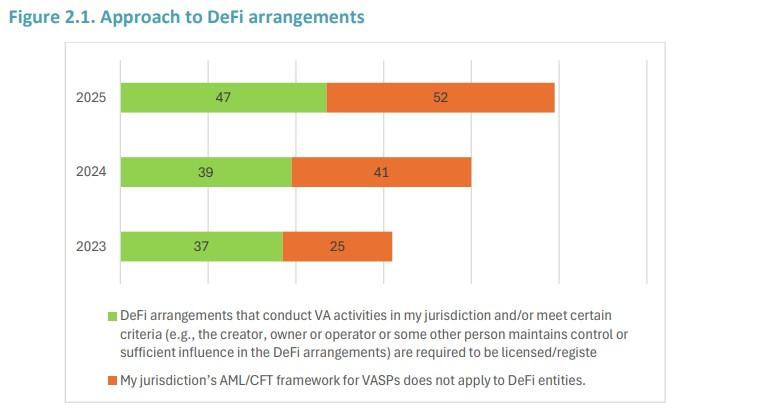

A June 2025 FATF report found regulators are still struggling to identify who actually controls or influences decentralized finance platforms.

The FATF discovered that 47 out of 99 countries with sophisticated regulations for crypto services mandate that specific DeFi platforms register as virtual asset service providers (VASPs), the identical classification applied to exchanges. However, among these 47 jurisdictions, merely 12 have successfully identified at least one unregistered DeFi platform satisfying VASP criteria.

Tax authorities monitoring jurisdiction shoppers

With DAC8 implementation proceeding throughout the European Union during 2026, lawmakers are establishing uniform standards for data collection from identifiable cryptocurrency enterprises operating at scale. This implies that centralized trading platforms and custody providers face the initial wave of compliance requirements.

Tax collection authorities are carefully observing AML progressions, where initiatives to categorize VASPs and establish accountability frameworks may ultimately result in expanded reporting mandates for cryptocurrency platforms.

Mangels explained that the OECD maintains an active focus on deterring regulatory arbitrage. Policy architects are continuously tracking whether cryptocurrency platforms attempt relocating operations to countries that have not yet adopted the CARF.

"A big part of my work at the OECD was tracking where crypto service providers were actually relocating. As new crypto centers are developed or come online, they will also be expected to comply with the OECD standards," Mangels said.

Although the OECD lacks direct enforcement authority, countries choosing to remain outside its framework typically encounter reputational damage and economic consequences, frequently intensified by FATF oversight measures.