February Could See Bitcoin Slide to $60K Based on Options Market Signals

The trajectory for Bitcoin appears limited below $70,000 as market participants embrace bearish options plays, while spot Bitcoin ETF withdrawals indicate a potential pullback to yearly lows.

Key takeaways:

- Market professionals are willing to spend a 13% premium to secure protection against downward price movement as Bitcoin fights to hold support levels beyond $66,000.

- Despite continued resilience in equity markets and gold valuations, Bitcoin ETF withdrawals totaling $910 million indicate growing wariness among institutional participants.

The Bitcoin (BTC) price trajectory shifted into decline mode following a rejection around the $71,000 mark on Sunday. Although the digital asset managed to preserve the $66,000 support threshold during the week, derivatives markets are showing increasing anxiety as seasoned traders position themselves to minimize exposure to downward price action.

Despite the fact that equity indices and gold valuations maintain their strength, market participants appear to be strategically positioning for a pullback toward $60,000 instead of panicking in response to short-term Bitcoin price declines.

Put options for Bitcoin (which give holders the right to sell) commanded a 13% premium compared to call options (which provide buying rights) on Thursday. When market conditions are neutral, this delta skew measurement ordinarily fluctuates within a -6% to +6% band, signaling equilibrium between bullish and bearish strategies. The persistence of these elevated readings throughout the previous four weeks demonstrates that institutional sentiment remains tilted strongly toward defensive positioning.

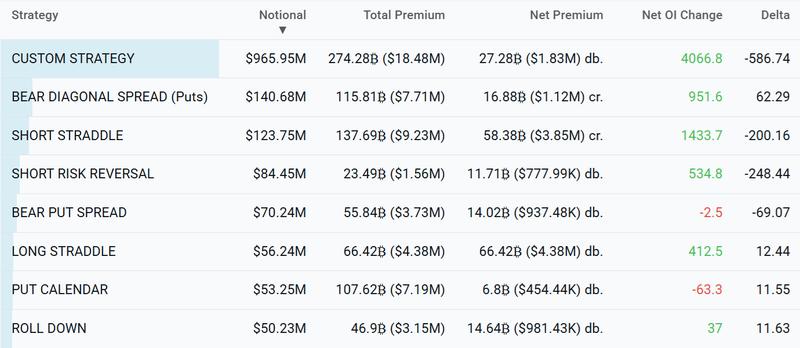

This pessimistic outlook becomes evident through the neutral-to-negative positioning observed within Bitcoin options markets. Data from Laevitas reveals that the bear diagonal spread, short straddle and short risk reversal emerged as the most actively traded approaches on Deribit's platform during the preceding 48 hours.

The bear diagonal spread strategy reduces the expense of betting on downward movement since near-term options depreciate more rapidly, whereas the short straddle achieves maximum profitability when Bitcoin's price remains relatively stable. In contrast, the short risk reversal produces gains from declining prices with minimal or zero initial capital outlay, though it exposes traders to boundless risk should prices surge unexpectedly.

Underwhelming institutional appetite for Bitcoin ETFs adds to market pessimism

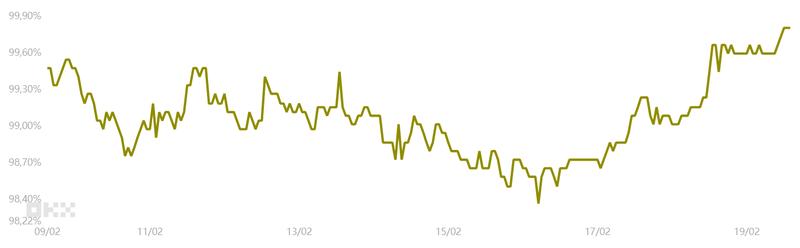

For a more comprehensive assessment of trader risk appetite, market analysts frequently examine stablecoin demand dynamics within China. During periods when investors scramble to liquidate cryptocurrency holdings, this metric generally falls beneath the parity threshold.

During balanced market conditions, stablecoins typically command a premium between 0.5% and 1% when measured against the US dollar/Yuan conversion rate. This markup accounts for elevated traditional foreign exchange conversion expenses, wire transfer charges, and the regulatory obstacles imposed by China's restrictions on capital movement. The present 0.2% discount points toward modest capital outflows, representing an enhancement from the 1.4% discount recorded on Monday.

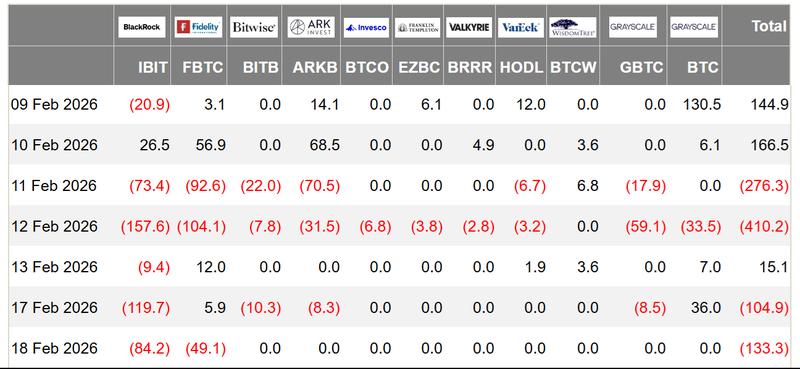

A portion of the prevailing dissatisfaction within the trading community stems from the disappointing activity levels in Bitcoin exchange-traded fund (ETF) products, which function as an indicator of institutional investment interest.

Bitcoin ETFs trading on US exchanges have experienced cumulative withdrawals amounting to $910 million starting from Feb. 11, a development that presumably surprised bullish investors—particularly given that Bitcoin was trading 47% beneath its record peak while gold quotations approached $5,000, representing a 15% appreciation over merely two months. In a similar vein, the S&P 500 index remained just 2% away from its historical high, suggesting that this risk-averse behavior is predominantly confined to the digital asset sector.

Although Bitcoin options markets telegraph apprehension regarding additional downward pressure, market participants are presumably maintaining exceptionally defensive positions until a definitive explanation for the dramatic plunge to $60,200 on Feb. 6 becomes apparent.