Institutional Retreat? Bitcoin Futures Open Interest Plunges to Lowest Point Since 2024

Bitcoin open interest has experienced consecutive monthly declines, yet options data suggests equilibrium between buyers and sellers. Is this evidence of institutional players reducing their cryptocurrency exposure?

Main highlights:

- Open interest in Bitcoin futures has dropped to its weakest point since 2024, indicating institutional traders are exercising heightened caution.

- While bullish sentiment appears diminished, substantial CME open interest indicates that leading institutional players remain active in the space.

The price of Bitcoin (BTC) has climbed 10% following a retest of the $63,000 threshold on Saturday, offering optimism to market bulls even as equity markets diverged amid growing Middle Eastern geopolitical tensions. Nevertheless, appetite for Bitcoin futures contracts has been waning, with open interest dropping to levels not witnessed since 2024. This development has sparked concerns among market participants that large institutional investors may be withdrawing from the cryptocurrency sector.

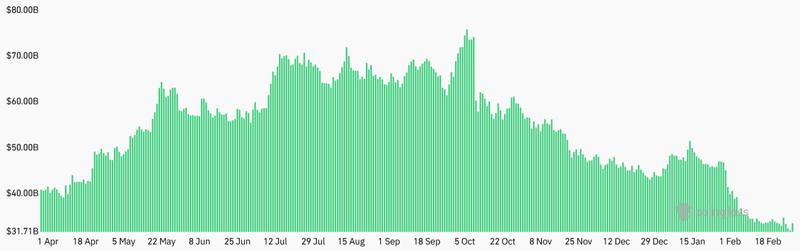

Open interest across major cryptocurrency exchanges for Bitcoin futures contracts fell to $32 billion on Sunday, representing a 20% decrease from the previous month. When calculated in Bitcoin units to account for recent price fluctuations, current BTC futures demand registers at 491,300 BTC, marking the weakest level observed since August 2024. A portion of this reduction can be attributed to forced liquidations affecting bullish traders who were unprepared for the downturn.

Appetite for leveraged long positions has remained notably subdued following the $126,200 record peak achieved in October 2025.

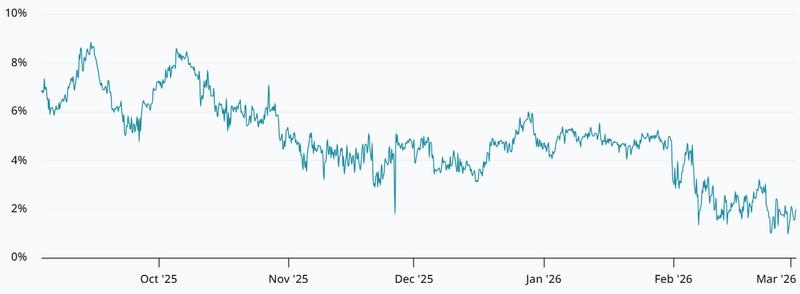

The annualized premium on Bitcoin monthly futures contracts, also known as the basis rate, has declined to 2%, its weakest reading in twelve months. In typical market conditions, this indicator should fluctuate between 5% and 10% to provide adequate compensation for the extended settlement timeframe. Adding to concerns is the basis rate's inability to maintain optimistic levels throughout the past year, a timeframe that encompasses a 50% price surge occurring between April and May 2025.

The cryptocurrency's lackluster performance compared to precious metals like gold and traditional equity markets has presumably redirected investor focus away from digital assets. Nevertheless, suggesting that institutional participants have completely abandoned the market would be an overreach, particularly considering that spot Bitcoin exchange-traded funds (ETFs) maintain average daily trading volumes exceeding $3 billion. The roster of ETF stakeholders includes several of the planet's most prominent mutual fund administrators and pension fund managers.

Additionally, publicly traded corporations currently hold more than $79 billion worth of Bitcoin in their onchain reserves, with notable holders including Strategy (MSTR US), MARA Holdings (MARA US), XXI (XXI US), and Metaplanet (MPLTF US). National governments such as Bhutan, El Salvador, and the United Arab Emirates have also established Bitcoin positions. While one might contend that institutional adoption still has considerable room for expansion, the current landscape remains substantially distant from nonexistent.

Derivatives data reveals market stability despite cautious bullish sentiment

Analysis of the Bitcoin options marketplace confirms that derivative instruments continue operating normally notwithstanding multiple unsuccessful attempts to recapture the $72,000 price threshold.

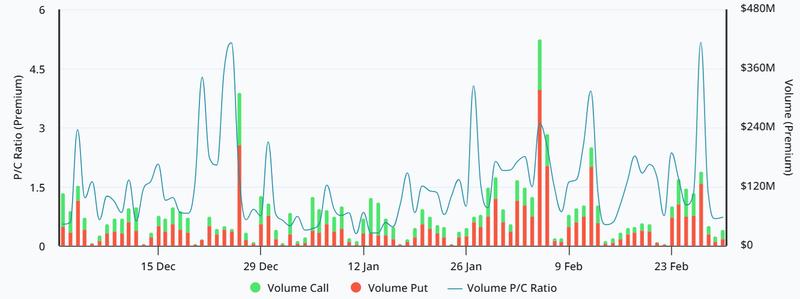

The put-to-call options premium for Bitcoin remained around 0.7 on Monday. This metric indicates that appetite for put (sell) options trails behind call (buy) options. A temporary spike in bearish strategy demand observed on Friday proved short-lived. In essence, options market dynamics reveal no indications of significant distress or persistent strain stemming from recent months' volatility.

Data from derivatives markets also reveals diminished confidence among bullish traders, particularly given that Bitcoin currently trades 45% beneath its historical peak. That said, concrete evidence supporting the notion of wholesale institutional departure remains absent. The $7.5 billion in Bitcoin futures open interest maintained on the CME exchange provides unmistakable confirmation of ongoing institutional participation. Regardless of selling pressure, each short (sell) position necessarily requires a corresponding long (buy) position, thereby maintaining market equilibrium.

Over time, anxiety and doubt dissipate as additional buyers reenter the market, signaling the conclusion of bearish trends. Although determining whether $60,000 represents the definitive floor for this market cycle remains uncertain, Bitcoin has once more demonstrated its resilience as a secure store of value with predetermined supply constraints. The $1.4 trillion cryptocurrency marketplace has validated its robustness and displays no indicators of systemic weakness.