Electronic tax form delivery for cryptocurrency proposed by IRS as new mandate

Should the proposal be approved, it will become effective on January 1 of the calendar year that follows the publication of the IRS's finalized regulations.

A new proposal from the United States Internal Revenue Service (IRS) aims to mandate that cryptocurrency exchange platforms deliver tax forms to their customers exclusively through electronic means.

According to existing regulations, cryptocurrency exchanges must furnish physical paper versions of tax form 1099-DA—the official IRS document used for recording cryptocurrency transactions conducted through a centralized platform or broker—whenever users make a request for paper-based forms.

The proposed regulatory changes, scheduled for publication this Friday, would eliminate this existing requirement and grant brokers the authority to "terminate" business relationships with current customers who decline to accept tax forms through electronic delivery methods.

Furthermore, under the IRS's new proposal, users would be prevented from retroactively withdrawing their consent to receive forms electronically.

The IRS mandates that all broker-dealers—platforms that provide cryptocurrency-related services to customers such as trading exchanges—must report customer proceeds generated from individual transactions and must supply customers with Form 1099-DA, which provides a comprehensive record of their trading activity for tax filing purposes.

Nevertheless, tracking cost basis will not be mandatory for exchanges during the 2025 tax year; the responsibility for tracking cost basis, which represents the original purchase price for each investment transaction, falls on the individual investor. The IRS detailed the reporting obligations for brokers in the following manner:

"Brokers required to make these returns must include identifying information of the customer, such as the customer's name and tax identification number (TIN), and such other relevant information, including the gross proceeds from the transaction."

Approximately one in five American citizens, representing roughly 55 million people, own digital assets within the United States, based on data from the National Cryptocurrency Association (NCA), an organization that advocates for the cryptocurrency industry.

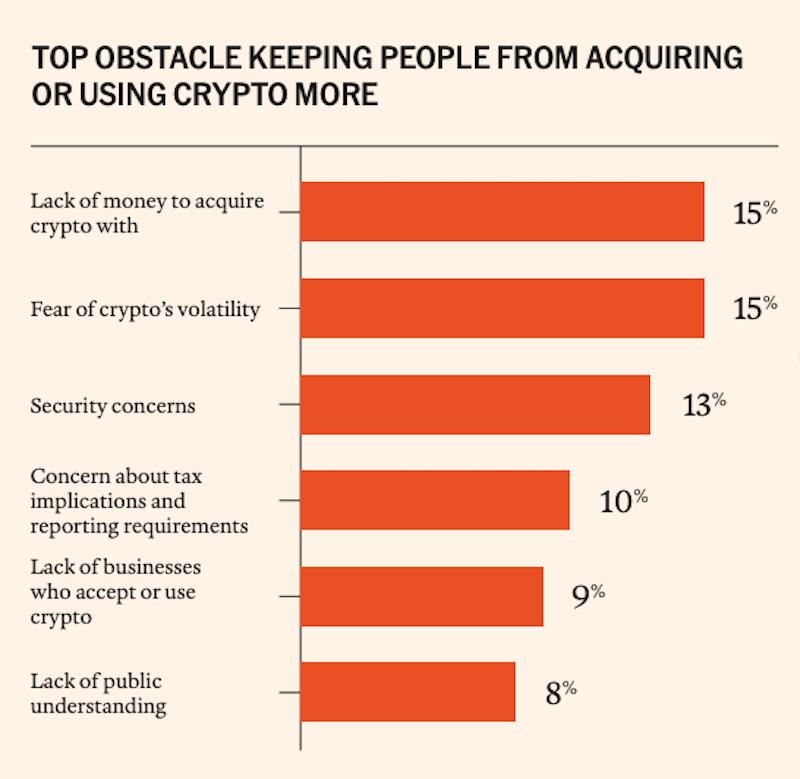

Compliance with tax regulations emerged as one of the most significant obstacles to cryptocurrency adoption, with 10% of the 54,000 survey participants in the NCA study identifying taxation of digital assets as a problematic concern.

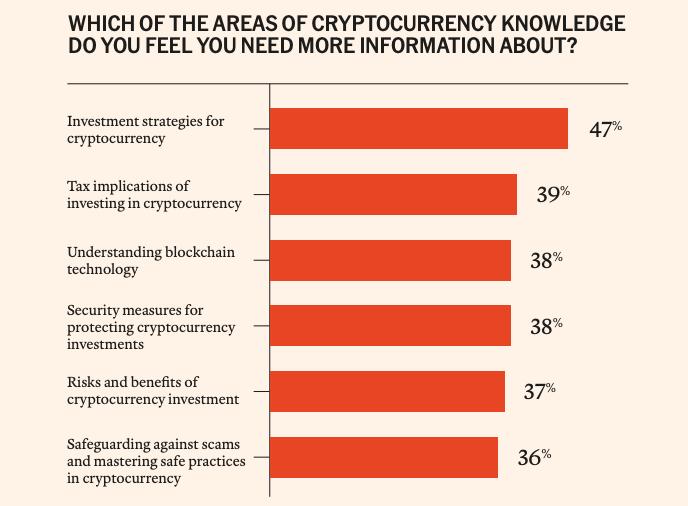

Over one-third of survey participants expressed a desire for additional educational resources regarding the tax consequences of holding and trading digital assets, based on findings from the NCA.

Concerns resurface after Trump killed the controversial "DeFi broker rule"

During December 2024, the IRS released a regulatory rule that designated all front-end service providers, which includes decentralized exchanges (DEX) and decentralized finance (DeFi) platforms, as broker-dealers, thereby making them subject to tax reporting obligations.

Under this classification, DeFi platforms would have been obligated to gather know-your-customer (KYC) data and submit reports to the IRS documenting proceeds from customer sales transactions.

In April 2025, US President Donald Trump put his signature on a resolution that eliminated the DeFi broker rule, a move that garnered positive reactions from participants in the cryptocurrency industry.

Despite this development, executives from the cryptocurrency sector have raised concerns regarding vague language contained in the currently stalled CLARITY market structure bill, which could potentially impose KYC reporting obligations on DeFi platforms and restrict operations in this emerging sector.