Bitcoin Payment Adoption: Examining Who Really Uses BTC for Transactions

While Bitcoin claims to be electronic currency, what percentage of holders actually make purchases with it? We analyze actual transaction statistics and identify genuine BTC payment scenarios.

Key takeaways

- Tracking genuine Bitcoin payment activity proves challenging since numerous transactions occur via third-party services, cryptocurrency-linked cards, or immediate fiat conversions.

- Research indicates a notable percentage of cryptocurrency owners have utilized digital assets for purchasing products or services on at least one occasion, though surveys typically don't differentiate Bitcoin from alternative cryptocurrencies.

- The El Salvador implementation demonstrates that granting Bitcoin legal tender status doesn't automatically translate to widespread daily consumer adoption, particularly when traditional payment infrastructure remains efficient.

- Statistics from payment processing platforms reveal cryptocurrency transactions occur more frequently within digital commerce and premium categories including tourism, technology products, and online services.

At the time Satoshi Nakamoto created Bitcoin, the vision centered on establishing digital currency. Yet, an important question remains: What number of individuals genuinely utilize Bitcoin for commercial transactions?

Finding a straightforward answer proves elusive. Transaction information exists in scattered fragments, numerous payments flow through third-party intermediaries, and an expanding segment of cryptocurrency-based commerce currently relies on stablecoins rather than Bitcoin (BTC). Nevertheless, examining survey results, processor statistics, application environments, and national-scale implementations can provide greater understanding.

This analysis shows that although Bitcoin has not yet achieved mainstream daily transaction usage, it finds application in circumstances where it addresses real-world challenges more effectively than conventional payment alternatives.

This piece examines the complexity of quantifying Bitcoin payment activity, insights from consumer research regarding spending patterns, lessons from El Salvador's Bitcoin adoption initiative, revelations from payment processor analytics, and scenarios where Bitcoin transactions deliver genuine practical value.

Why measuring Bitcoin payments is harder than it seems

No centralized global database exists that comprehensively records Bitcoin usage at point-of-sale terminals. When attempting to quantify Bitcoin transaction activity, researchers rely on alternative measurement approaches:

- Population surveys questioning whether individuals have completed cryptocurrency-based purchases

- Transaction volume statistics from payment processing companies serving merchants

- Government initiatives designating Bitcoin as official currency

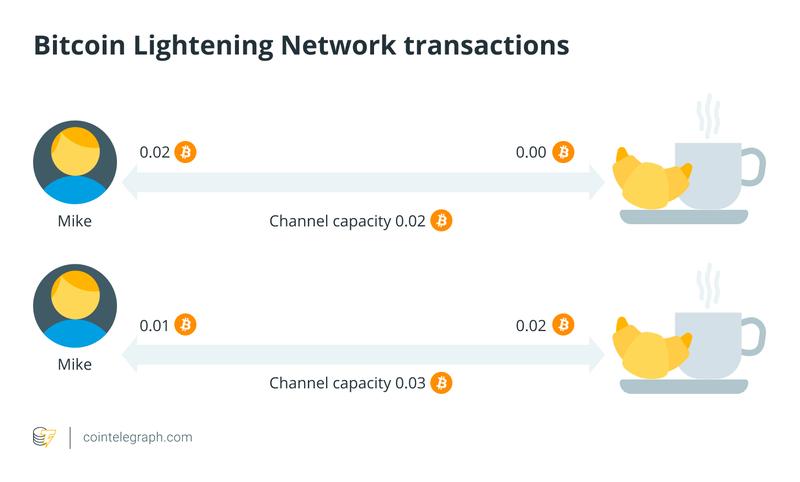

- Application-based platforms facilitating Lightning Network transactions.

- Lightning payments are a way to send Bitcoin instantly for a negligible fee. It works like a high-speed express lane on top of the main Bitcoin network, making it suitable for small everyday purchases.

Multiple elements contribute to the complexity of accurately measuring Bitcoin payment volume:

- Businesses typically don't retain the Bitcoin they accept. Processing platforms frequently execute immediate conversions from BTC to traditional currency, enabling merchants to eliminate exposure to price fluctuations. While the customer's perspective records a Bitcoin transaction, the merchant's accounting reflects standard currency receipt.

- Cryptocurrency-backed payment cards obscure the boundary between Bitcoin transactions and traditional purchases. When individuals utilize Visa cards funded by digital assets, merchants process fiat currency through conventional banking infrastructure. This represents cryptocurrency-funded spending rather than authentic Bitcoin payment settlement.

- Stablecoins dominate an increasing proportion of cryptocurrency payment activity. Digital tokens maintaining fiat currency pegs, especially dollar-denominated versions, constitute significant transaction volume across both commercial payments and international money transfers.

These considerations make it valuable to recognize three distinct transaction categories:

- Direct Bitcoin payments executed onchain or via Lightning Network infrastructure

- Bitcoin payments that undergo automatic fiat conversion during processing

- Transactions utilizing alternative digital assets, including stablecoins.

Did you know? In 2010, 10,000 BTC was used to buy two pizzas, marking the first known commercial Bitcoin transaction and proving that the network could be used for real-world trade, not just peer-to-peer transfers.

What surveys suggest about spending habits

Within the population of cryptocurrency owners, spending activity occurs with moderate frequency but lacks consistency.

According to a 2025 National Cryptocurrency Association survey, 39% of crypto holders reported using cryptocurrency to shop for goods and services.

Research from GM Global Cryptocurrency Insights, conducted in 2024, 11% of respondents reported actively using crypto for purchases, while 19% expressed interest in using crypto for everyday transactions.

Survey results demonstrate that a meaningful proportion of cryptocurrency holders have completed at least one purchase transaction using digital assets. However, these studies generally fail to distinguish Bitcoin from alternative cryptocurrencies and don't measure transaction frequency.

This distinction carries significance. An individual who executed a single cryptocurrency payment for airline travel or digital services appears statistically identical to someone making frequent purchases, despite substantial differences in their contribution to payment system adoption.

El Salvador: A real-world test for Bitcoin payments

El Salvador represents the sole nation to establish Bitcoin as officially recognized legal tender across its territory, providing a unique environment for evaluating everyday payment adoption.

Notwithstanding initial promotional programs implemented after Bitcoin received legal tender designation in 2021, consumer adoption throughout the country failed to achieve substantial growth. Only a small percentage of the population incorporated it into routine transactions, and the majority of businesses accepting BTC documented minimal transaction volumes.

Multiple factors account for this outcome:

- Price volatility created challenges for both buyers and sellers in establishing stable pricing.

- Numerous users rapidly converted government-distributed incentives into traditional cash.

- Business owners lacked strong motivations to actively promote Bitcoin payment acceptance.

- Technical usability barriers remained problematic for non-expert users.

The El Salvador implementation illustrates that official legal recognition alone fails to establish widespread consumer payment behaviors, particularly when established payment methods operate effectively.

Initially, the country mandated Bitcoin payment acceptance for private sector businesses. Nevertheless, during early 2025, businesses received authorization to determine their Bitcoin acceptance policies independently as part of an arrangement with the International Monetary Fund (IMF). Bitcoin payment functionality remains legally valid for government obligations including tax payments and public service fees.

Did you know? In certain countries, Bitcoin kiosks allow users to pay utility bills by converting BTC into local payment networks, turning crypto into an indirect but practical payment bridge.

What payment processors show about actual usage

Cryptocurrency payment processing services provide visibility into commercial merchant transaction activity. Several recurring trends emerge:

- Online commerce generates higher transaction volumes compared to brick-and-mortar retail locations.

- Typical transaction values frequently exceed standard retail purchase amounts.

- Product categories including tourism services, premium merchandise, digital subscriptions, and consumer electronics demonstrate increased prevalence.

These observed patterns correspond with fundamental economic principles. Cryptocurrency payments deliver enhanced value for substantial international payment transfers.

An additional developing pattern shows stablecoins representing a substantial percentage of cryptocurrency-based commercial payments. Merchants encounter simplified accounting and currency conversion processes when receiving dollar-denominated tokens compared to maintaining Bitcoin holdings.

Although cryptocurrency payment adoption continues expanding within merchant processing infrastructure, Bitcoin's proportional contribution to this activity may represent less than the majority, across both business-to-business (B2B) and peer-to-peer (P2P) transaction categories.

Lightning and app-based payment systems

For Bitcoin to function effectively as everyday transaction currency, Lightning Network infrastructure plays a critical role. Lightning facilitates instantaneous, minimal-cost payments, enabling economically viable small-value transactions.

However, Lightning simultaneously introduces additional measurement complexities. Numerous transactions remain outside the primary blockchain ledger, making comprehensive volume tracking difficult.

What becomes observable instead focuses on platform-level activity.

Applications exist that enable Lightning Network functionality, permitting users to complete merchant payments without maintaining direct Bitcoin custody. Within certain implementations:

- Users initiate payment using traditional currency.

- The application executes cryptocurrency conversion automatically.

- Merchants receive Bitcoin settlement through Lightning infrastructure.

From the merchant perspective, this qualifies as Bitcoin payment receipt. From the user experience, it may simply resemble scanning a standard QR code.

This methodology obscures conventional definitions of Bitcoin payment transactions, yet it holds importance by reducing technical friction.

Did you know? Nonprofits have started using Bitcoin donations to receive funds globally within minutes, especially when traditional wire transfers or card payments face regional shutdowns.

Where Bitcoin payments actually make sense today

Available data collections and practical examples indicate that Bitcoin payment utilization concentrates primarily within particular economic sectors rather than broad-based consumer retail activity:

- Cross-border small business payments: International sellers, digital commerce operators, and independent contractors occasionally select Bitcoin to circumvent international banking delays, capital controls, or substantial intermediary charges. Rapid settlement and transaction finality outweigh volatility concerns since currency conversion occurs promptly.

- Travel and high-value online purchases: Flight reservations, accommodation bookings, and technology products frequently feature in cryptocurrency payment analytics. These represent scenarios where payment card processing fees become substantial and international customer bases are typical.

- Donations and censorship-resistant funding: Charitable organizations, advocacy movements, and humanitarian initiatives employ Bitcoin when conventional payment infrastructure proves unreliable or faces political restrictions.

- Remittances in certain corridors: Stablecoins dominate most cryptocurrency-based remittance volume, though Bitcoin maintains relevance where local conversion services exist and recipients can execute exchanges efficiently.

- Gift card and voucher systems: Numerous individuals utilize Bitcoin through purchasing retail gift cards or prepaid value certificates indirectly. This doesn't constitute direct merchant acceptance, yet it represents legitimate consumer spending methodology.

- Local circular economies: Concentrated communities surrounding Bitcoin enthusiast gatherings, tourism destinations, or shared workspace environments can exhibit localized adoption. These instances are authentic but remain limited in overall scope.

So, how many people actually pay with Bitcoin?

No precise worldwide figure exists for Bitcoin payment transaction volume, and any specific user population estimate warrants skepticism.

Available evidence substantiates these conclusions:

- Within cryptocurrency holder populations, a considerable minority has executed cryptocurrency-based purchases, though regular usage patterns remain uncommon.

- Daily Bitcoin transaction adoption for routine purchases has stayed minimal, including within nations that actively promoted adoption.

- Merchant acceptance infrastructure exists, though payment volume concentrates within specific industry verticals and geographic markets rather than widespread retail penetration.

- An expanding proportion of cryptocurrency-based commercial payments currently employs stablecoins instead of Bitcoin, especially for business transaction settlement.

Bitcoin operates currently more as specialized payment technology infrastructure than as universal consumer transaction currency.

Practical milestones for Bitcoin adoption

Future advancement of Bitcoin as a mainstream payment mechanism will probably rely less on theoretical benefits and more on practical infrastructure development.

Critical progress indicators worth monitoring include:

- User applications that abstract cryptocurrency wallet management and private key handling from end users

- Merchant integration tools that incorporate Lightning functionality without operational complexity

- Transparent regulatory frameworks governing cryptocurrency payment settlement procedures and financial accounting

- Competitive dynamics between Bitcoin-based systems and stablecoin payment networks.

Should Bitcoin payment execution become as straightforward as scanning a QR code within established applications, usage adoption may accelerate, contingent upon regulatory developments and market evolution.