Banking Sector Faces Genuine Risk from Stablecoin Expansion, Standard Chartered Warns

Regional banking institutions in the United States face significant exposure as stablecoin expansion threatens to siphon deposits, according to Standard Chartered analyst Geoff Kendrick.

According to fresh research from Standard Chartered's analytical team, stablecoins represent a genuine threat to banking deposits on both a global scale and within United States borders.

The postponement of the CLARITY Act in the United States — proposed legislation that would ban the payment of interest on stablecoin holdings — serves as a "reminder that stablecoins pose a risk to banks," stated Geoff Kendrick, who leads digital assets research globally at Standard Chartered, in a Tuesday report reviewed by Cointelegraph.

"We estimate that US bank deposits will decrease by one-third of stablecoin market cap," Kendrick noted, referencing the $301.4 billion marketplace of stablecoins pegged to the US dollar, according to data from CoinGecko.

The research from Standard Chartered contributes additional perspective to the ongoing CLARITY Act discussion, occurring as entities such as Coinbase have pulled their support, while Circle's CEO Jeremy Allaire has characterized concerns about bank runs triggered by stablecoins as "totally absurd."

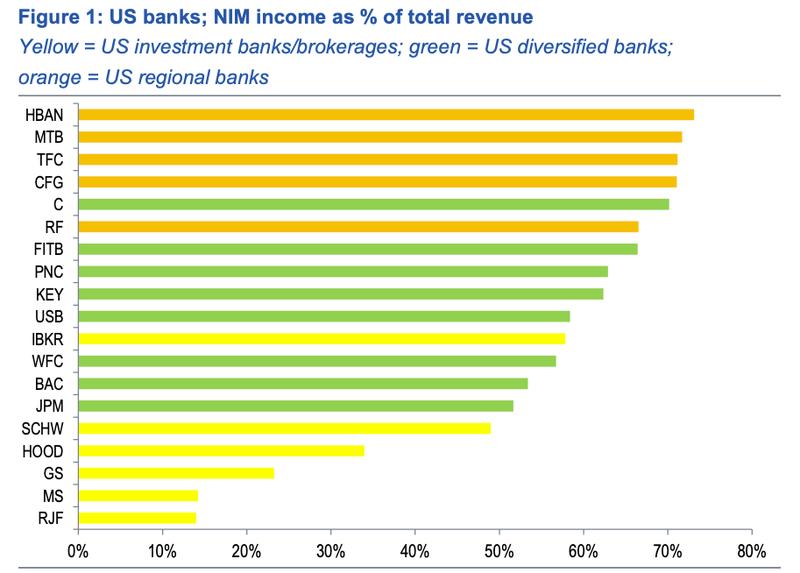

Regional US banks most exposed, investment banks least

Within the research document, Kendrick drew attention to net interest margin (NIM) income — an essential profitability indicator that calculates the gap between interest revenue earned and interest expenses paid, then divides this by average assets that generate interest.

"NIM income as a percentage of total bank revenue is the most accurate measure of this risk because deposits drive NIM, and they risk leaving banks as a result of stablecoin adoption," Kendrick explained.

"We find that regional US banks are more exposed on this measure than diversified banks and investment banks, which are least exposed," the analyst continued, identifying Huntington Bancshares, M&T Bank, Truist Financial and CFG Bank as institutions facing the highest exposure levels.

The volume of US banking deposits vulnerable to stablecoin adoption hinges on multiple variables, encompassing the geographical location of issuer deposits, demand from domestic versus international sources, and wholesale versus retail demand patterns, according to the analyst's observations.

Tether and Circle hold just 0.02% and 14.5% of reserves in bank deposits

Should stablecoin issuers maintain a substantial portion of their deposits within the banking infrastructure of the jurisdictions where their stablecoins are distributed, the likelihood of bank runs would diminish, Kendrick explained in his report, further stating:

"The idea is that if a deposit leaves a bank to go into a stablecoin, but the stablecoin issuer holds all of its reserves in bank deposits, there would be no net deposit reduction."

That said, Tether and Circle — companies behind the planet's two most prominent stablecoins, USDt (USDT) and USDC (USDC) — maintain merely 0.02% and 14.5% of their respective reserves in banking deposits, Kendrick's report revealed, with the analyst noting: "So very little re-depositing is happening."

Examining domestic versus international demand patterns, Kendrick determined that demand originating domestically depletes local banking deposits, whereas foreign-sourced demand does not produce this effect.

"We estimate that around two-thirds of stablecoin demand comes from emerging markets at present, so one-third comes from developed markets," the analyst documented.

Kendrick further elaborated that, using a forecasted $2 trillion market capitalization as a baseline, approximately $500 billion in deposits might depart from developed-market banking institutions before the close of 2028, with an estimated $1 trillion potentially exiting emerging-market banking systems during the same timeframe.

The analyst also indicated that Standard Chartered maintains its expectation for the CLARITY Act to achieve passage before the conclusion of the first quarter of 2026. Kendrick emphasized that risks associated with bank runs extend beyond stablecoins alone, but also originate from the "inevitable" proliferation of real-world assets in the digital finance ecosystem.