Central Bank Digital Currencies: A Powerful Tool for Expanding Access to Financial Services

Digital currencies issued by central banks offer solutions for 1.3 billion people without bank accounts, helping close the gap between cash-based and digital economies. Active government support can position CBDCs as affordable, secure pathways to mainstream financial systems.

Opinion by: Xin Yan, co-founder and CEO of Sign.

The lack of access to financial services continues to be among the most enduring obstacles confronting governments worldwide. Data from the World Bank reveals that over 1.3 billion adults globally lack access to banking services and do not possess a financial account. This population depends entirely on physical currency, resulting in a 'cash-digital divide' that marginalizes them from participating in the mainstream economic system.

Closing this gap requires governments to champion CBDCs with vigor. Being a government-backed, secure substitute for paper money, CBDCs represent optimal tools for reaching financially marginalized communities. By providing a frictionless gateway into the broader financial landscape, widespread CBDC implementation serves as a crucial accelerator and core building block toward achieving comprehensive financial access for all.

Expanding participation in financial institutions plays a critical role in driving national economic expansion. When more individuals engage in investment activities and join the mainstream economy, the overall capital pool grows larger, resulting in enhanced financial security. Additionally, integrating people into the regulated economy guarantees that monetary policy adjustments benefit the broader population, strengthens government supervision and reduces fraudulent activities.

The majority of individuals in lower-income brackets prefer cash-based transactions because physical money is straightforward to utilize, universally recognized, comes without processing fees and serves as a reliable form of payment.

The systems required to manage physical currency create a barrier separating the unbanked segment from mainstream economic participation.

Financial inclusion as government policy

Creating physical infrastructure to administer, safeguard and process cash in distant areas demands substantial resources. This explains why numerous service providers choose not to offer financial solutions dependent on cash due to elevated operating costs.

Physical currency exchanges additionally fail to generate digital footprints, creating a data shortage for providers of financial services. As a result, organizations categorize the complete unbanked segment as high-risk clients, blocking their entry to insurance products and lending markets.

The unavailability of cost-effective digital payment options and the missing transaction records undermine financial health and impede a nation's economic development. Under these circumstances, universal availability of mainstream financial products becomes a priority for government leadership.

Certain monetary authorities view financial accessibility as a fundamental aspect of their responsibilities and implement strategies to guarantee universal participation in the mainstream economy. With this objective, various central banks have explored launching CBDCs to expedite the development of an accessible financial infrastructure.

CBDCs can accelerate financial inclusion

Based on a 2023 research paper by Kosse and Mattei cited by the IMF, approximately 60% of developing and low-income nations identify financial accessibility as among their top three reasons for launching a CBDC. The strong belief in CBDCs derives from their characteristics that make them the perfect connection to mainstream economic systems for populations without banking access.

CBDCs have the capability to function through a dual-tier distribution framework. This framework enables traditional banks along with alternative financial entities to serve the financially marginalized population. Beyond widening the financial system's coverage, non-traditional intermediaries reduce the substantial overhead expenses associated with conventional brick-and-mortar banking operations.

Given that a considerable share of the unbanked demographic lacks reliable internet access or cellular network coverage, the capability to transact without connectivity becomes essential. Industry specialists have observed how CBDCs are being engineered to incorporate strong offline functionality. Investigating promising technologies for proximity-based communication guarantees dependable CBDC transactions in isolated regions experiencing connectivity limitations.

Being a government-operated digital platform, CBDCs are constructed with a focus on societal benefit rather than financial gain. By eliminating the excessive overhead associated with traditional intermediary structures, CBDCs facilitate a highly streamlined expense framework.

Rather than facing heavy fees, participants enjoy minimal transaction expenses that are negligible, guaranteeing the system stays both available to those without banking access and financially sustainable for the government authority issuing it.

Furthermore, the underserved population has greater likelihood of placing confidence in CBDCs as a digital substitute for cash since they receive support from a trustworthy institution. In contrast to the liquidity limitations of commercial financial organizations, CBDCs will perpetually remain a direct obligation of the central bank, rendering them comparatively secure.

Perhaps most significantly, CBDCs offer an entry point for the financially marginalized population to engage in the regulated economy. This occurs through the seamless transfer of transaction information between CBDCs and the wider financial services sector.

CBDCs have the capacity to facilitate privacy-protecting information exchange, permitting participants to willingly share their payment records to establish credit ratings for accessing deposit accounts, lending products, and insurance offerings.

When formal credit records are absent, financial institutions can utilize CBDC payment information as a valid resource to assess financial conduct and loan eligibility. Service providers would consequently possess the ability to evaluate a client's risk characteristics and confirm identity to provide lending products and additional financial solutions.

Toward CBDC mass adoption

CBDC utilization depends on technological knowledge, power supply infrastructure, and availability of compatible devices. Information demonstrates that countries have already achieved substantial advancement across all these dimensions.

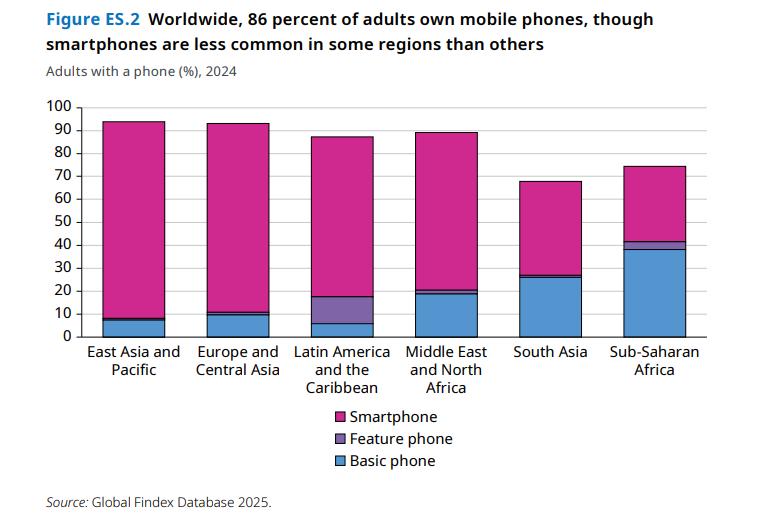

The 2025 Global Findex Database published by the World Bank Group has documented that 86% of adults currently possess a mobile phone. Furthermore, 79% of adults presently hold a bank account, and 61% are conducting digital transactions throughout low and middle-income nations.

The report notably indicates that "despite high mobile phone ownership and growth in account ownership, 1.3 billion people still lack financial accounts." This segment of the population possesses mobile devices, identification documents, and SIM cards, which represent the requirements for a digitally accessible account.

Nevertheless, they continue to be financially marginalized from the regulated economy.

Under these conditions, CBDCs stand as one of the key offerings that can deliver secure, economical, and accessible financial products to end-users.

Monetary authorities and national governments need to implement a comprehensive strategy and leverage CBDCs to assist the financially unfamiliar population in connecting with the mainstream economy.

Opinion by: Xin Yan, co-founder and CEO of Sign.