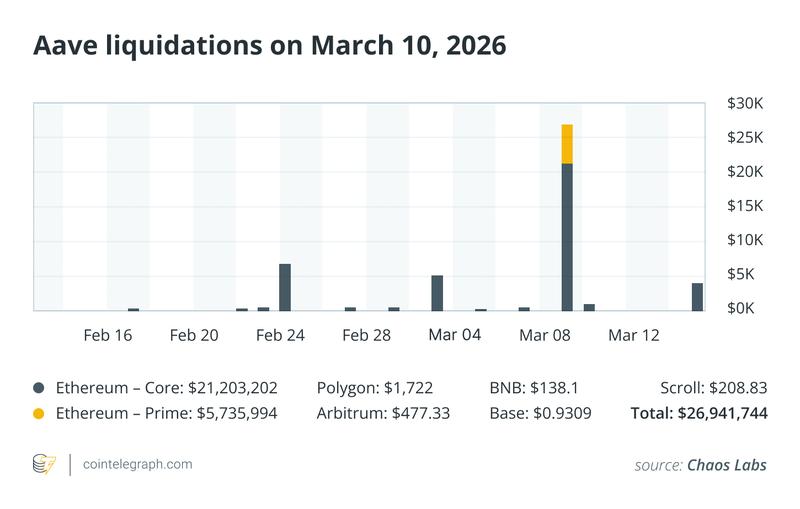

$27 Million in Aave Liquidations Sparked by Minor 2.85% Oracle Error

An insignificant wstETH collateral pricing miscalculation led to $27 million in liquidations across Aave, underscoring the vital importance of accurate price oracles and automated risk management infrastructure in decentralized finance.

Key takeaways

- An ephemeral 2.85% price variance in wstETH collateral values initiated approximately $27 million worth of liquidations across Aave's platform, demonstrating how seemingly minor technical glitches can produce substantial financial ramifications within automated DeFi lending ecosystems.

- The mass liquidation event unfolded when Aave's infrastructure momentarily assessed wstETH at roughly 1.19 ETH rather than its actual market price hovering around 1.23 ETH, causing multiple borrowing positions to register as inadequately collateralized.

- Decentralized finance relies heavily on price oracles as foundational infrastructure components that deliver external marketplace data to blockchain-based smart contracts, establishing collateral valuations, determining loan viability and triggering automated liquidation events.

- The underlying problem stemmed not from defective price data feeds but rather from an improper configuration within Aave's CAPO risk oracle infrastructure, where stale smart contract settings generated a temporary restriction on the token's permissible exchange rate.

Protocols operating in decentralized finance (DeFi) employ automated mechanisms to manage all aspects of operations, from maintaining collateral to evaluating risk exposure. This architecture facilitates a genuinely permissionless and accessible financial infrastructure, yet it simultaneously creates scenarios where seemingly insignificant technical malfunctions can escalate into serious financial upheavals.

Data from Chaos Labs, a specialized risk monitoring organization, indicates that a market decline occurring on March 10, 2026, resulted in roughly $27 million in liquidated positions among Aave protocol users, vividly demonstrating this susceptibility. Within a 24-hour period, user positions totaling approximately $27 million underwent forced liquidation. Remarkably, the trigger was not an enormous market collapse but instead a transient 2.85% price variance impacting wrapped staked ETH (wstETH) used as collateral.

This incident underscores the indispensable nature of reliable price oracles and comprehensive risk management architectures for maintaining stability throughout the DeFi landscape.

This analysis examines how a mere 2.85% valuation error in wstETH collateral assets catalyzed approximately $27 million in forced liquidations on Aave's lending infrastructure. It demonstrates how oracle setup choices, smart contract configuration details and automated liquidation protocols can magnify minor pricing inaccuracies across DeFi marketplaces.

An unexpected wave of forced liquidations

As liquidations swept through Aave's various markets, Chaos Labs, which continuously monitors lending platforms for anomalous behavior patterns, rapidly detected and highlighted the unusual activity. Initial conjecture among market watchers suggested a potential breakdown in the price oracle infrastructure, possibly causing incorrect valuation of collateral holdings within the platform.

Oracle systems function as vital connectors, delivering external marketplace pricing information to blockchain-based smart contract applications. Within lending platforms such as Aave, these data streams establish whether borrowers maintain adequate collateral backing for their outstanding loans. Should collateral valuations drop beneath mandatory thresholds, the protocol initiates automated liquidation procedures for affected positions.

The collateral token central to this particular incident was wstETH, a widely adopted asset throughout DeFi lending platforms.

Did you know? Forced liquidations on protocols like Aave typically execute more rapidly than conventional margin calls. Since DeFi marketplaces function continuously through automated smart contract systems, positions can face liquidation within mere seconds after collateral ratios breach minimum required levels.

Understanding wstETH

The token known as wstETH, representing wrapped staked Ether (ETH), originates from Lido protocol operations, a prominent liquid staking service provider.

Users who stake Ether through Lido's platform initially obtain stETH tokens, representing their staked ETH combined with accumulated staking rewards. For enhanced compatibility across diverse DeFi protocols, stETH undergoes wrapping into wstETH format.

Because staking rewards continuously accumulate, each wstETH token typically maintains a value marginally exceeding one ETH. This characteristic renders it an especially desirable and extensively utilized collateral form throughout DeFi lending ecosystems.

The valuation discrepancy explained

Throughout the liquidation episode, a divergence emerged between wstETH's genuine market valuation and the price calculation employed by Aave's risk management infrastructure. Aave's computational systems assigned wstETH a value of roughly 1.19 ETH, while marketplace participants valued it nearer to 1.23 ETH.

This approximately 2.85% disparity resulted in positions backed by wstETH appearing more severely undercollateralized than their actual status.

Consequently, specific borrowing positions dropped beneath their mandatory safety margins, activating Aave's automated liquidation procedures.

The critical importance of price oracles throughout DeFi

Oracle systems constitute fundamental infrastructure throughout decentralized finance. Blockchain networks lack inherent capabilities to retrieve real-world market information, necessitating oracle services to furnish external price data for various assets. These information feeds directly determine:

- collateral asset valuation

- the financial health status of borrowing positions

- determinations regarding when liquidations become necessary

An indicated decline in collateral pricing can cause the protocol to classify a loan as inadequately secured, initiating automated liquidation of that position.

Since this process operates through algorithmic logic, even relatively small pricing variations can multiply into considerable repercussions.

Did you know? Minor price variations can generate disproportionate impacts across DeFi platforms. Even temporary oracle or market price deviations of merely several percentage points can initiate cascading liquidation events. This vulnerability intensifies when numerous borrowers maintain highly leveraged positions secured by volatile cryptocurrency collateral.

Identifying the actual culprit: CAPO risk-oracle configuration error

Comprehensive investigation verified that Aave's principal price oracle infrastructure was functioning correctly.

The fundamental problem actually originated within the correlated assets price oracle (CAPO) risk oracle module, an supplementary protective mechanism applied to specific asset types.

CAPO was expressly engineered to impose limits on the rate at which valuations of yield-generating tokens such as wstETH can appreciate. This protective measure shields the protocol against sudden price spikes or potential oracle manipulation attempts.

However, during this particular event, a configuration discrepancy within CAPO systems precipitated the difficulty.

Technical analysis of the malfunction

Chaos Labs revealed that the defect emerged from obsolete configuration values preserved within a smart contract.

Two essential data points had diverged from proper synchronization:

- the baseline exchange rate reference

- the timestamp associated with that particular rate

Since these values were not updated simultaneously, CAPO calculated a transient maximum on the permitted exchange rate that fell beneath the current market valuation.

This discrepancy caused the protocol to underestimate wstETH's value by roughly 2.85% compared to its actual market price.

Did you know? Aave's functionality depends on price oracle systems, which are information feeds delivering real-time asset pricing data to smart contract infrastructure. When these feeds momentarily reflect abnormal market valuations from trading platforms, the protocol automatically recalculates collateral worth and may initiate liquidation procedures.

The cascading liquidation phenomenon

Immediately upon collateral ratios declining below mandatory thresholds, Aave's automated liquidation infrastructure engaged.

Professional liquidators, predominantly high-frequency trading algorithms, intervened by settling portions of borrowers' outstanding debt and, as compensation, obtaining the underlying collateral assets at an incorporated discount.

Throughout this event, approximately $27 million in outstanding borrowing positions underwent liquidation.

Liquidation participants ultimately secured roughly 499 ETH in aggregate profits and liquidation incentives, exploiting the brief pricing misalignment.

Protocol avoided accumulating bad debt

Despite the substantial liquidation volume, Aave maintained zero bad debt throughout the incident. Stani Kulechov, Aave founder, confirmed that there "was no impact to the Aave Protocol."

According to Chaos Labs, the platform's fundamental risk management and liquidation systems operated as originally programmed once positions violated their safety parameters. When positions crossed their threshold limits, liquidations executed according to their intended design.

The disturbance consequently remained limited to impacted individual borrowing accounts and posed no danger to the protocol's comprehensive solvency or operational stability. The resulting artificial suppression in collateral valuation forced multiple borrowing positions beneath their liquidation trigger points.

Aave's governance structure proposed compensating affected participants through reimbursements financed by recovered funds and decentralized autonomous organization (DAO) treasury resources. This methodology reflects an emerging trend throughout DeFi governance structures, where protocols progressively treat technical incidents as systemic infrastructure vulnerabilities. They may proceed to compensate impacted participants rather than requiring them to absorb permanent financial losses.

Highlighting oracle vulnerability in decentralized finance

This incident emphasizes that oracle architecture continues representing one of the most essential and susceptible components of DeFi infrastructure.

Even relatively minor configuration errors can initiate disproportionate outcomes when automated systems supervise billions of dollars in collateral assets.

Similar incidents have materialized across alternative DeFi platforms. As an illustration, an improperly configured oracle previously valued Coinbase's wrapped staked ETH (cbETH) temporarily at approximately $1 rather than its actual price near $2,200, generating extensive disruption.

These occurrences emphasize the persistent difficulties of sustaining dependable, precise price information feeds throughout decentralized financial infrastructures.

wstETH and Lido bore no responsibility

Representatives from the Lido ecosystem clarified that the liquidation events did not originate from any defect or malfunction in wstETH token mechanics.

The token performed normally throughout the entire incident, and Lido's underlying staking protocol infrastructure remained completely operational and unaffected.

The central issue evidently originated from how Aave's lending protocol processed and evaluated pricing information through its proprietary risk management configuration settings.

Forward-looking lessons for decentralized finance

As the decentralized finance sector continues expanding, protocols are implementing progressively advanced risk management frameworks to accommodate yield-bearing assets like wstETH.

These asset types introduce distinctive pricing complexities because their valuations increase progressively over time through accruing staking rewards.

Robust risk modeling systems must consequently appropriately manage:

- fluctuating exchange rates

- continuous accumulation of staking rewards

- time-dependent parameter updates

- accurate synchronization of smart contract configuration values

Even slight inconsistencies among these components can intensify into extensive liquidation incidents.