Major Knowledge Gaps Persist Among Crypto Investors Regarding Tax Obligations, Coinbase Study Reveals

Joint research by Coinbase and CoinTracker reveals that less than 50% of cryptocurrency holders have accurate knowledge about when their digital currency holdings trigger tax liabilities.

Fresh research indicates that a significant portion of cryptocurrency holders continue to grapple with fundamental concepts related to tax obligations, despite the fact that the majority express their intention to remain compliant with regulations.

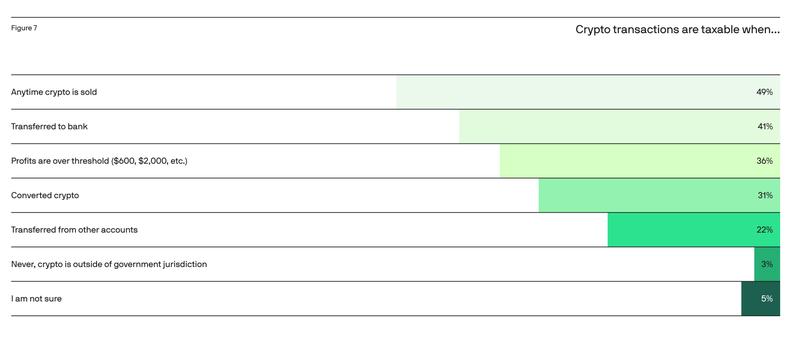

Just 49% of those surveyed correctly identified that cryptocurrency triggers taxable events upon sale, whereas close to 25% mistakenly think that merely transferring assets between wallets can create tax liabilities, as reported in the 2026 Crypto Tax Readiness Report jointly released by Coinbase and CoinTracker.

The data was gathered through a comprehensive survey involving 3,000 cryptocurrency users based in the United States, which took place between Sept. 9 and Oct. 3, in preparation for the upcoming 2025 tax filing period.

According to the survey results, cryptocurrency holders demonstrate a strong commitment to tax compliance, with 74% acknowledging their awareness that digital assets are subject to taxation, and 65% confirming they have previously filed reports of their crypto-related transactions. "This refutes the misconception of widespread crypto tax avoidance," the survey states.

New IRS rules complicate tax reporting

The research also highlighted several significant obstacles that make cryptocurrency tax filing more complex. A primary issue is that digital asset holders typically maintain their holdings across numerous platforms, averaging 2.5 different wallets or exchange accounts, with 83% utilizing self-custody solutions. Such distribution of assets across multiple platforms creates difficulties in maintaining accurate cost basis records, which are essential for properly computing capital gains and losses.

Recently implemented reporting requirements further compound these difficulties. Starting with the 2025 tax year, brokerage platforms will be required to issue Form 1099-DA, however, these forms will not contain cost basis information, placing the burden on individual users to manually reconcile their transaction histories across various platforms that do not share information with one another.

In spite of these complications, the majority of cryptocurrency users continue to depend on conventional solutions for tax preparation. Approximately 78% utilize mainstream tax preparation software and 52% seek assistance from professional accountants, whereas a mere 8% employ cryptocurrency-specialized tax services. Concurrently, there is increasing enthusiasm for artificial intelligence applications, with nearly half of survey participants indicating they would be willing to use AI for tax calculations and 30% expressing openness to depending on it for handling their complete tax filing process.

IRS moves to mandate digital crypto tax forms

In recent weeks, the IRS put forward new regulatory guidelines that would make it mandatory for cryptocurrency trading platforms to provide tax documentation exclusively through electronic means, eliminating the availability of physical paper forms. According to the proposed regulations, brokerage firms would have the authority to terminate business relationships with customers who decline electronic delivery, and users would be unable to revoke their consent after initially providing it.

Trading platforms will be required to continue providing Form 1099-DA for reporting transaction proceeds, although the tracking and documentation of cost basis will continue to be the obligation of individual investors.