Traditional Banking Struggles to Accommodate Cryptocurrency Despite Growing Acceptance

While digital currencies gain legitimacy in financial markets, cryptocurrency investors continue to face account restrictions and blocks from traditional banking institutions.

Throughout the world, cryptocurrency holders continue to encounter frozen bank accounts and blocked transactions, despite the fact that institutional acceptance of digital assets is on the rise.

Panos Mekras, the co-founder and CEO of blockchain fintech firm Anodos Labs, started working with cryptocurrency in Greece during the late 2010s. At that time, the majority of Greek banking institutions prohibited transfers to cryptocurrency trading platforms. Mekras encountered numerous blocked card transactions until he eventually found a single bank that would allow his transfers, though not before being interrogated to confirm he comprehended he was dealing with a "risky" counterparty.

In his conversation with Cointelegraph, Mekras explained that these initial rejections represent how banking institutions categorize digital currencies as fundamentally high risk. Such categorization frequently resulted in account terminations or unexpected freezes with no warning, which eventually forced his company to depend entirely on onchain infrastructure and payment systems.

The public's view of cryptocurrency has transformed since then. Today, crypto is experiencing a rebranding effort, transitioning from a purely speculative investment vehicle to a foundational infrastructure for tomorrow's financial instruments. Despite this shift, Mekras noted he continues to face identical banking obstacles, with incidents occurring as recently as a "few months ago":

"I tried to send money from an exchange to Revolut, and they froze my account for three weeks. I had no access to my [funds] during that time."

The long shadow of crypto debanking

Mekras is far from the only cryptocurrency owner voicing such grievances, even as banking institutions announce their expansion into digital asset custody and blockchain projects.

A report released in January by the UK Cryptoasset Business Council discovered that banking transfers to cryptocurrency exchanges were experiencing blocks or delays, with approximately 40% of transactions facing restrictions and 80% of trading platforms reporting heightened friction throughout the previous year.

The council issued a warning that wholesale prohibitions and transaction caps are frequently implemented without consideration for whether the exchange operates legally.

According to the UK council's research, Revolut represents one of just two banking institutions that allow both wire transfers and debit card usage, and it also happens to be the platform where Mekras alleges his most recent account suspension occurred. The company functions as an authorized UK banking entity "with restrictions," indicating it is presently developing its banking infrastructure ahead of a full-scale launch. Additionally, it maintains a European Union banking license through Lithuania and provides cryptocurrency trading features within its application.

A representative from Revolut informed Cointelegraph that the company approaches account freezes as a "last-resort" protective measure for customers in accordance with Anti-Money Laundering (AML) and Know Your Customer (KYC) requirements.

"A temporary freeze may occur if our systems detect irregular activity. This could be a combination of a few factors, such as if a customer interacts with a platform frequently exploited by fraudsters, or we believe that the funds in question may be the proceeds of crime or sanctions circumvention," the spokesperson said.

The company representative further stated that beginning Oct. 1, merely 0.7% of Revolut customer accounts that received cryptocurrency deposits were subject to restrictions or freezes following an investigation.

When banks close doors, users move onchain

Within certain geographic areas, cryptocurrency faces outright prohibition, leaving users subject to far more severe limitations. Cryptocurrency on- and off-ramps are not legally available in areas such as China, forcing users to turn to peer-to-peer (P2P) marketplaces or underground markets to exchange crypto.

Although China represents the most extreme case on the spectrum, other countries have reduced both official and unofficial barriers. Nigeria previously prohibited cryptocurrency and even restricted P2P trading platforms. Nevertheless, the country formally acknowledged digital assets as securities in 2025.

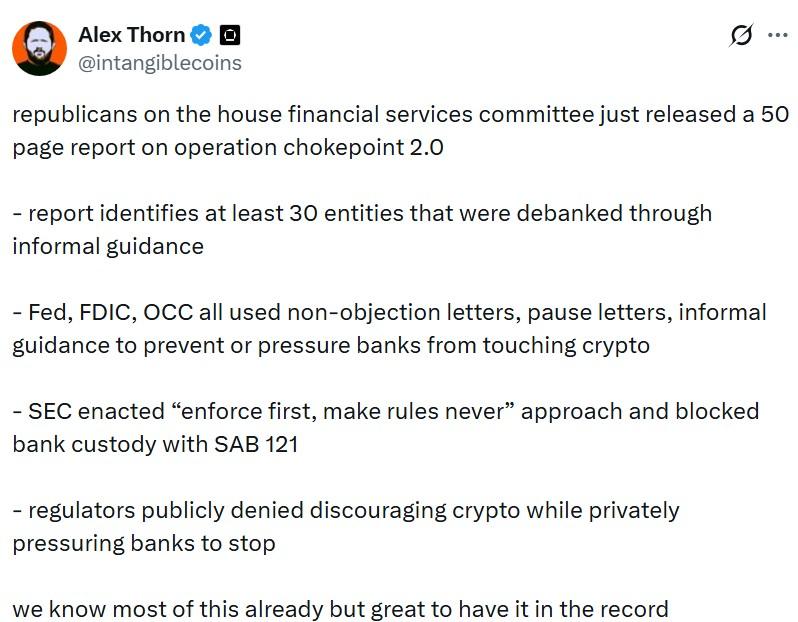

Comparable banking resistance patterns have also surfaced in the US. Politicians and industry participants have employed the phrase "Operation Chokepoint 2.0" to characterize the federal regulators' unofficial guidance that deterred banks from continuing relationships with cryptocurrency businesses.

The initial "Operation Choke Point" represented an initiative where enforcement authorities were criticized for compelling banks to sever connections with politically controversial sectors including payday lending operations and firearms dealers.

Donald Trump assumed office as the president of the US in January 2025 and has been advocating for cryptocurrency-supportive policies aimed at establishing the world's largest economy as the "crypto capital" of the planet.

Issues surrounding crypto debanking have subsequently received official acknowledgment. In December, the US Office of the Comptroller of the Currency (OCC) published its conclusions regarding debanking practices conducted by nine of the nation's largest banking institutions. The OCC additionally released an interpretive letter to verify that banks are permitted to facilitate cryptocurrency transactions in a broker-like role.

Despite the encouraging progress, users continue to voice complaints that the banking industry refuses to service accounts that have cryptocurrency exposure.

"This is still the case [and] there are still anti-crypto positions. Some have even said publicly that they are not willing to support crypto activity or engage with the industry," said Mekras.

Mekras contended that users might consider completely disconnecting from the conventional banking infrastructure and transferring their finances onchain. While this sounds feasible in principle, in practice, the majority of businesses and individual users still cannot function purely within the cryptocurrency ecosystem without dependable access to traditional fiat currency channels.

Banking's turn toward blockchain infrastructure

Over recent years, a worldwide transformation has occurred in how conventional financial entities interact with cryptocurrency.

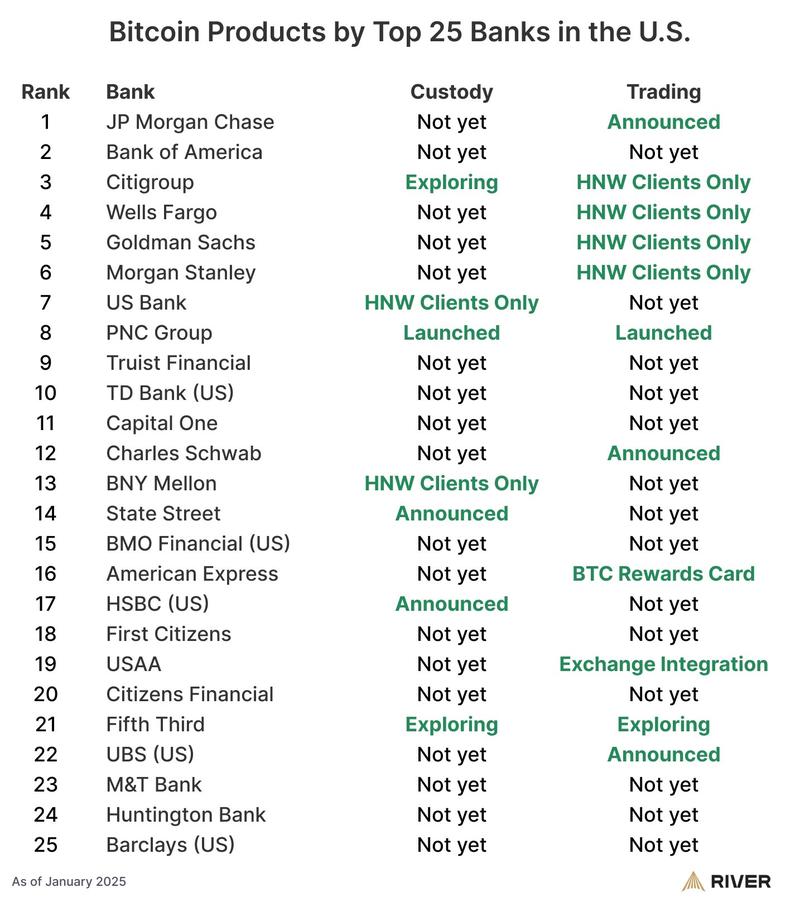

Leading banks and financial infrastructure providers are progressively developing products and solutions connected to Web3. Within the US, 60% of the nation's top 25 banking institutions are reportedly providing or developing Bitcoin-related offerings, encompassing custody, trading and advisory services.

Throughout Europe, regulated offerings such as cryptocurrency custody and settlement are being rolled out by established exchanges and financial conglomerates operating under the Markets in Crypto-Assets Regulations (MiCA). In the UK, HSBC's blockchain infrastructure was chosen to facilitate pilot programs for tokenized government bond issuances.

Against this context of institutional integration, certain companies working to connect banks with blockchain technology assert that the difficulties resulting in account freezes are connected to technological gaps and risk assessment frameworks within banking institutions.

"The problem is that there's a huge amount of friction because traditional banks don't really have the internal infrastructure to interpret blockchain data in a way that fits inside their existing risk and compliance frameworks," Eyal Daskal, CEO of Crymbo — a blockchain infrastructure platform for institutions — told Cointelegraph.

He characterized the circumstances as a scenario where banking institutions frequently resort to preventative actions because they lack the capability to connect onchain transactions with the identity verification and compliance indicators they depend upon:

"If crypto is involved, they block the account and treat it as out of scope. It's the simplest option for them because they don't have the tools to assess it properly."

Cryptocurrency is making its way into the mainstream financial system, yet for numerous users, obtaining basic banking services remains contingent upon whether a bank's risk assessment system can comprehend blockchain activity. Until this technological and procedural divide is bridged, the industry's institutional acceptance and retail-level friction are likely to persist simultaneously.